Investment Strategy Team Davy Private Clients

Irish Outlook 2017 - Strong recovery but challenges ahead

10th January, 2017

Most countries use Gross Domestic Product (GDP) as the main measure for analysing trends in their underlying economies and, given the improvement in statistical techniques, commentators agree it provides a fairly accurate description of those trends in most cases.

Distorted by multinationals

Not so for Ireland. For many years now measures of Irish GDP have been distorted by the accounting policies of a small number of multinationals which account for a relatively small portion of the overall economy. Very often, therefore, estimates of GDP growth have given a misleading impression of underlying trends in the broader economy. The most striking example is the latest estimate by the Central Statistics Office (CSO) that real GDP increased 26% in 2015, an estimate that spawned the phrase “leprechaun economics” from many commentators. Therefore, we must examine a broader group of variables in Ireland to a get a sense of the underlying direction. When we do this there is compelling evidence that the Irish economy recovered strongly in 2015 and 2016.

In the transport sector there was a sharp increase in car and commercial vehicle sales, as well as a significant increase in traffic volumes. Almost two-thirds of the 300,000 net jobs lost in the 2008 to 2012 recession have been recouped and the unemployment rate has halved. Non-car retail spending also recovered strongly as did output in the traditional industrial sectors, which excludes multinationals. Most commentators estimate underlying growth in the economy of between 4% and 5% in 2015 and 2016, well short of the 26% official estimate, but still very impressive by international standards.

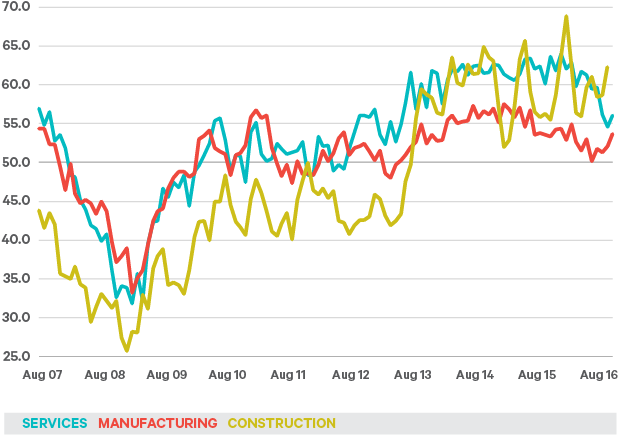

More recent evidence suggests that the pace of growth has slowed in recent months. The Purchasing Managers’ Indices (PMIs) have fallen from their lofty highs, retail sales were flat over the summer months and output growth in traditional industries has slowed again. This is neither surprising nor worrying. The early stages of recoveries from very deep recessions can produce large percentage increases but as previous peaks are reached, there is a natural and welcome slowing in the rate of growth.

Figure 1: Purchasing managers' indices remain strong

Source: Bloomberg

We estimate the underlying rate of growth in the economy over the next year or so will be of the order of 4%. If achieved, that would represent a very satisfactory outcome.

Brexit

However, as always there are challenges and uncertainties. Some are international but others are specific to the Irish economy. The Brexit referendum result and the election of Donald Trump as US president were predicted by a small minority of commentators. But the reaction of markets and economies, to date at least, has been more favourable than many financial analysts predicted.

In 2017 the focus may switch to Europe where general elections are scheduled in France, Germany, the Netherlands and, most likely, Italy. The Brexit referendum result and Trump’s victory illustrated a shift in support by the so-called 'disaffected' and a move away from traditional and established centre parties to more extremes on the left and right of the political spectrum. Many of these parties want to remove their currencies from the Eurozone and some wish to leave the European Union (EU). Clearly either would be destabilising.

A challenge closer to home is Brexit. To date the main impact has been a weakening of sterling against the euro, although some of this was subsequently reversed as political concerns moved to mainland Europe. It will be several years before the ultimate outcome is known and any estimates at this stage of the quantitative impact on Ireland are highly speculative, if not nonsensical.

Public sector pay

Two significant domestic issues that threaten the recovery in the economy are public sector pay and the housing shortage. The recent generous award by the Labour Court to An Garda Síochána has triggered fears of similar claims in other parts of the public service. The award occurred despite public service pay levels which already compare favourably with other sectors.

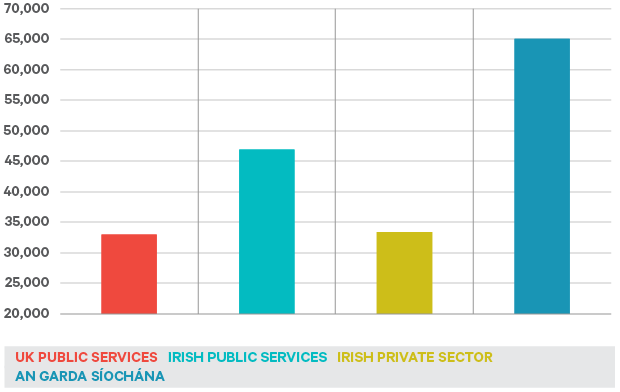

Average public sector pay in Ireland is substantially higher than the equivalent average in the UK and 40% higher than average pay levels in the private sector. Interestingly, An Garda Síochána is by far the highest paid broad group in the public service. Figure 2 shows that the average pay in An Garda Síochána is almost 40% higher than the rest of the public sector and almost double that of the private sector.

Figure 2: Average earnings for private and public sector compared

Source: Davy, CSO

Nevertheless, the recent award will almost inevitably trigger catch up claims, which is one of biggest challenges for the government this year if the recent improvement in the public finances is to be maintained.

The housing shortage

It now looks likely that house completions in 2016 were somewhere between 14,000 and 15,000 – a welcome increase on the 12,666 house completed in 2015. However, it is less than 50% of some estimates of the natural demand for housing, particularly as net inward migration has resumed after a period of significant net outflows during the recession.

Housing was established as a key priority by the new government last summer and Minister Simon Coveney produced a major action plan ‘Rebuilding Ireland’ to address the issue. While some of the proposals are welcome – particularly the proposal to restart a direct building programme – they fail to materially address the key issues in the rental and purchase market.

Since the bottom of the market, house prices and rents have risen by 50%. It is now expensive to buy or rent. Yet the supply of new houses is 50% below the natural demand and the supply of rental properties is at its lowest point since records began in 2006.

It is costly to buy and costly to rent, but not sufficiently attractive for developers or landlords to increase supply. The explanation of this dilemma is the very substantial cost between the buyer and the seller. Until we introduce measures which will reduce this “wedge” between buyers and sellers, housing will be a serious constraint from a social and economic perspective in 2017 and beyond.

WARNING:MarketWatch - Outlook 2017: New world order - This article is from our latest edition of MartketWatch, an in depth report focusing on the economic and political outlook for 2017.

WARNING: Past performance is not a reliable guide to future performance. The value of investments and of any income derived from them may go down as well as up. You may not get back all of your original investment. Returns on investments may increase or decrease as a result of currency fluctuations.