Let's talk about your retirement number

Request a call today to discuss your retirement number

Paula Finlay Director of Pensions, Davy Private Clients

27th September, 2019

Today, we are lucky enough to be living longer, healthier lives than previous generations. And for many of us, retirement is not seen as the beginning of the end but a new beginning. Travel, further education, a new career path, different business interests, family time - the post-work world is your oyster. How do you make the most of it all?

For almost every client we work with, whether in a company pension scheme, self-employed or a professional, the secret to a fulfilling retirement is planning. Not necessarily saving, or sacrificing, or working hard although of course, they come into it too – but thinking and planning ahead. Some of the things I ask every client up front is ‘How financially secure do you want to be when you retire. What’s your retirement number?’

This hypothetical figure is the starting point for most of our conversations about retirement. It focuses the mind. What level of assets or core capital do you need to accumulate over your working life in order to secure the level of retirement you want? Get that number down on paper first, and work from there. It’s a given that the planning process excludes your family home and/or ’rainy day’ fund. These are not considered part of your core capital and you should take little or no risk with them.

A traditional view is to take 66% of your final working salary and add the State pension, bringing you to around 70% of your final salary. To make things more accurate however, you should also take into account your current level of spending, along with any expenses that won’t be there when you retire (childcare costs, mortgage payments).

Let’s run a quick simulation.Someone retiring aged 65 and planning to spend around €50,000 per year after tax will today require a core capital fund of at least €1 million, to support their lifestyle over 25 years1 There is an alternative – purchasing this income as an annuity for life – however that would cost about €3 million from a life company2.

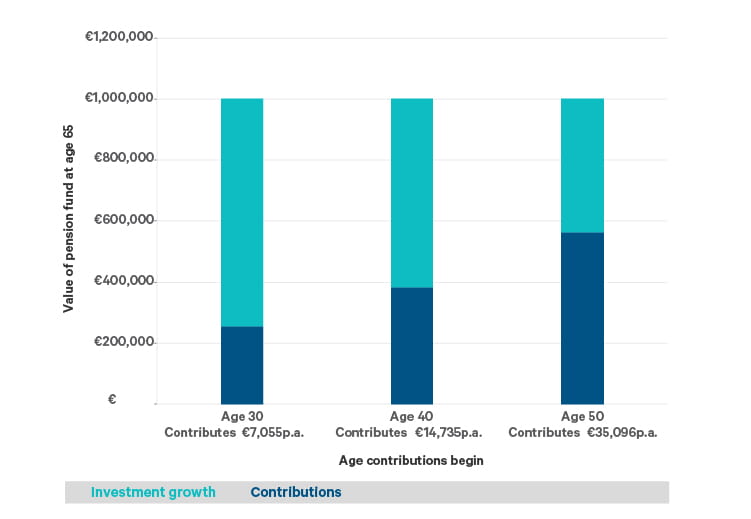

Now you’re asking the right question. Actually, starting a plan is the most important retirement step you’ll ever take. And as the following example illustrates, the sooner you start, the better.

In our example we have three individuals who are targeting a pension fund of €1m at age 653. Our early-starting 30-year-old needs to contribute just €7,055p.a. whereas our further-down-the-track

50-year-old has to contribute circa. €35,000p.a. to achieve the same result. A pretty remarkable difference in contributions.

Figure 1: Contributions required when targeting a pension fund of €1m

Source: Davy

Source: Davy

Investing in a pension over the long term and contributing to it regularly or ‘religiously’ also springs to mind. This is undoubtably the most tax efficient way to build up a nest egg. Not only do you get income tax relief on your contributions, but the income and gains within the pension fund can roll up free of income tax, CGT (capital gains tax) and fund exit tax.

Making regular contributions to your pension fund is the bare minimum – but on its own, it’s not enough. You also need to invest your fund so that it generates a further return on your investment. Before you take this step, however, you should have a good financial plan in place that is tailored to your personal circumstances and built around, amongst other things, your specific retirement objectives.

It’s worth taking time out to develop this plan because it will frame the decisions you make about how much you want to invest in your pension now, in the future and what you want to get out of your retirement fund. Some questions to pose: Will you have to pay education costs for children? At what age do you want to access your retirement fund? Do you envisage yourself continuing to have a hand in running your business after retirement age?

Once you have your plan in place, you can then decide how best to invest the fund with your retirement objectives in mind. To succeed over time, an investor needs to stick to the plan and let their investment portfolio do the work. One of the advantages of having a pension portfolio is that it is a long-term investment. It can cope with dips in the market and is more likely to recover and generate positive returns for you over the longer term.

Taking the time to even begin to think about your retirement goals might sound like an overwhelming task, which often means it’s an easy one to put on the ‘long finger’. That’s where we come in.

Spending just 60 minutes with a Davy adviser can provide enough information for us to begin to draw up your financial plan. This can be as simple as ensuring you start making regular pension contributions and give you the option of reviewing your pension investment strategy from time to time, ensuring it fits with your retirement objectives. Whether you are in a company pension scheme, self-employed or a professional we can develop a strategy to suit your circumstances. The bottom line is the same. The sooner you start, the better it gets.

To discuss how you might find your retirement number and then make it work, please request a call today.

1 Assumes inflation of 2.5%, returns net of fees of 6.5% and fund exit tax annually of 41%. 2 Based on an annuity rate of 1.578%, male, age 65, married, rate obtained 04/09/19. 3 Assumes 6.5% growth, not inflation adjusted.

Request a call today to discuss your retirement number

Warning: The value of your investment may go down as well as up. If you invest in this product you may lose some or all of the money you invest.

Warning: These figures are estimates only. They are not a reliable guide to the future performance of this investment.

Warning: The information in this article does not purport to be financial advice and does not take into account the investment objectives, knowledge and experience or financial situation of any particular person. You should seek advice in the context of your own personal circumstances prior to making any financial or investment decision from your own adviser. The tax information contained in this article is based on Davy’s current understanding of the tax legislation in Ireland and the Revenue interpretation thereof. It is provided by way of general guidance only and is neither exhaustive nor definitive and is subject to change without notice. It is not a substitute for professional advice. You should consult your tax adviser about the rules that apply in your individual circumstances. Davy is not responsible for the interpretation of this information and any submissions made by you or a third party on your behalf thereon.

Paula Finlay Director of Pensions, Davy Private Clients

Request a call today to discuss your retirement number