See the full potential

In inflationary times, doing nothing could be your riskiest move.

Fiona Haughey Associate Director, Financial Planning, Davy Private Clients

10th April, 2024

Pretty much everyone will need to keep cash for some reason. Whether its ensuring expenses can be met from income, or failing that knowing money is there to meet any cash shortfall now or in the future gives peace of mind. There are times though when more detailed discussions and advice are required on the topic. For example, a retiree who has received their pension lump sum and wants to discuss their options, a professional who has sold stock and is debating if repaying debt or investing the proceeds is best for them, or a successful business owner who is looking to optimise the accumulating cash in their business. In inflationary times, doing nothing could be your riskiest move. We offer a broad range of investment and liquidity solutions.

On the surface it may look risk free, but there are drawbacks to holding too much cash and for too long.

Cash certainly gives you options. However, we have viable options in liquidity solutions for the first time in more than a decade for money offering close to the European Central bank rate. Any decision around holding cash versus investing should incorporate your financial goals within a financial plan unique to your own circumstances. Cash can be a decent short-term solution for meeting short term expenses. For medium- and long-term goals we should look to more appropriately aligned solutions.

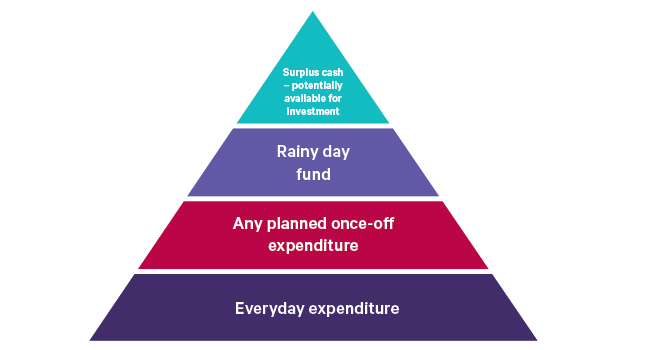

Source: Davy

1 Source: CSO CPI February 2021 to February 2024

In inflationary times, doing nothing could be your riskiest move.

Warning: The information in this article is for illustrative purposes only and does not purport to be financial advice as it does not take into account the investment objectives, knowledge and experience or financial situation of any particular person. You should seek advice in the context of your own personal circumstances prior to making any financial or investment decision from your own adviser. There are risks associated with putting a financial life plan in place. There is no guarantee that by having a financial life plan in place, you will meet your objectives.

Fiona Haughey Associate Director, Financial Planning, Davy Private Clients

In inflationary times, doing nothing could be your riskiest move.